Blog

Going forward with prudent fiscal management

The third quarter of 2022 is approaching an end. The epidemic is still changing fast and impacting on Hong Kong's economy, but the situation has become more stable when compared to the first half this year. The value of retail sales rebounded year-on-year in July. The unemployment rate had dropped from a high of 5.4% in February to April to 4.3% in May to July, with the total number of unemployed persons having fallen from some 200 000 to under 170 000. The improving labour market is expected to last when unemployment figures for June-August are released this week. Notable improvements to the employment of grassroots workers in such industries as retail, catering, etc. have also been observed.

This said, the economy as a whole has been plagued by the epidemic and a weak external market. Merchandise exports had registered negative growth, and the stock and property markets softened. Many enterprises, particularly small to medium-sized enterprises (SMEs), are still enduring pressure on their business operations. The rental enforcement moratorium implemented earlier this year was an exceptional measure under exceptional circumstances, and it played a key role in preventing massive closures of SMEs during the height of the local epidemic.

As the epidemic gradually came under control and domestic economic activities improved, the Government would need to adjust the approach of supporting the economy. Following the end of the rental enforcement moratorium period at the end of July, we have enhanced support for the Special 100% Loan Guarantee under the SME Financing Guarantee Scheme (SFGS) and the Pre-approved Principal Payment Holiday Scheme (PPPHS). This includes, among other things, work by the Hong Kong Monetary Authority (HKMA) and the Hong Kong Mortgage Corporation to strengthen the communication between banks and SMEs as well as industry associations to expedite the processing of corporate loan applications.

|

To alleviate the cash flow pressure on SMEs during the epidemic, I announced in the Budget earlier this year to enhance the Special 100% Loan Guarantee by increasing the maximum loan amount per enterprise, equivalent to the total sum of wages and rentals for 27 months; raising the ceiling to HK$9 million, relaxing the repayment period to a maximum of 10 years; and extending the application period for the scheme till the end of June 2023. At a time when the epidemic is gradually coming under control but the economy has yet recovered, these enhancements would allow enterprises to receive liquidity support. Since the launch of the Special 100% Loan Guarantee from April 2020 and till the end of August this year, around 55 000 applications involving loans of around $103 billion have been approved, benefiting approximately 33 000 enterprises which employed about 350 000 employees.

Both the Special 100% Loan Guarantee and PPPHS are designed specifically to assist enterprises hard hit by the epidemic in coping with cash flow pressure. Together with other relief measures, such as concessions or reductions in profits tax, rates, water and sewage charges, rentals or fees applicable to government properties, as well as the Consumption Voucher Scheme, we endeavour to support enterprises on multiple fronts so that they could survive in a market of fierce competition.

Last Friday, HKMA announced the extension of PPPHS for three months, from November to the end of January next year. The principal payment holiday period under SFGS (including the Special 100% Loan Guarantee), would be extended accordingly to a maximum of 36 months in total. On the same day, the Government announced further extension of rental or fee concessions applicable to government properties and short-term tenancies, etc. for three months, effective from October to December. In the meantime, the Government would holistically review the measures concerned and examine suitable subsequent arrangements. We will make announcements at the appropriate juncture.

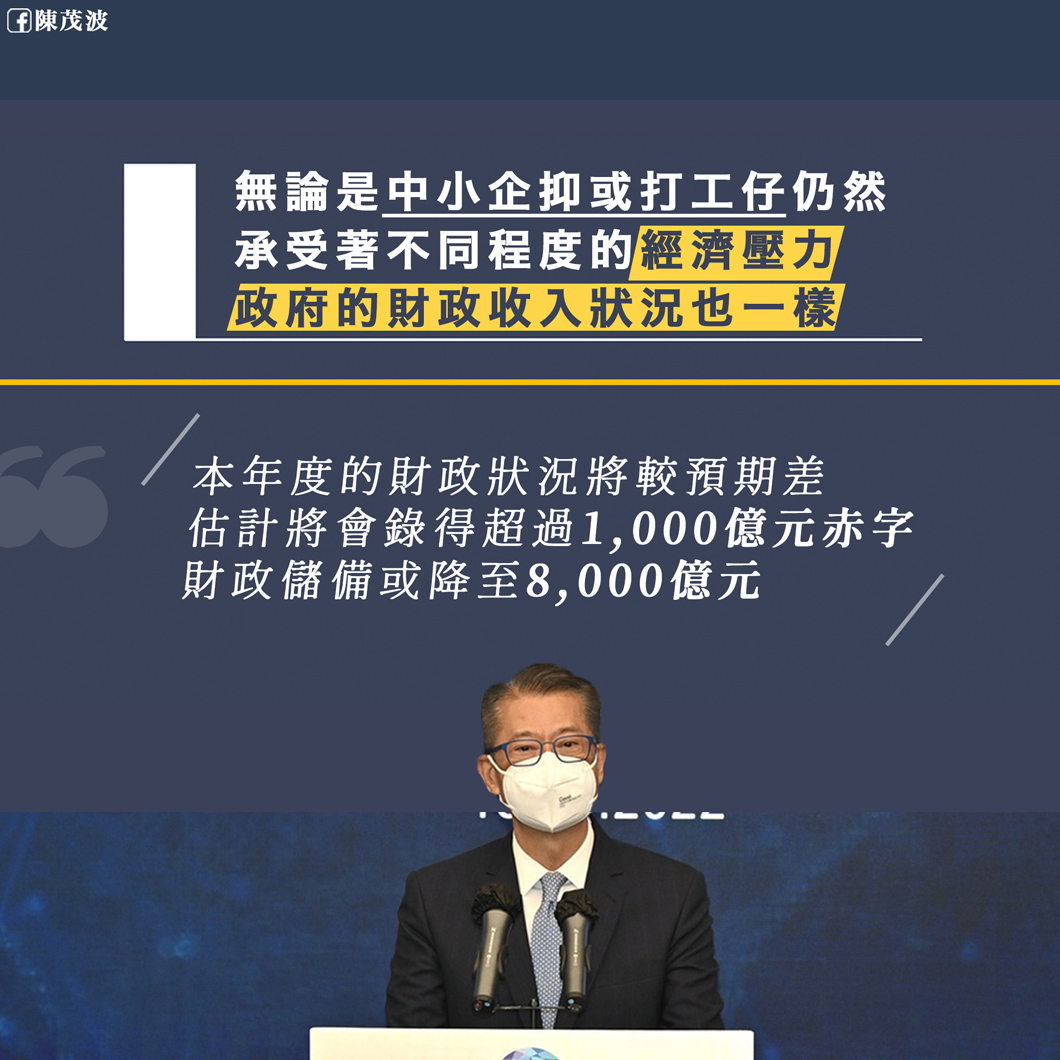

Indeed, just as SMEs and wage earners alike are facing varying degrees of economic pressure, the Government's revenue position is also under stress. It is reasonable to assume that in a sluggish economy, government revenue would fall short of expectations, while expenditure would rise. Under such circumstances, the fiscal position for the 2022-23 financial year would be worse than originally anticipated. We are expecting a deficit of over $100 billion, far above the estimated amount of $56.3 billion in the Budget this year. If this becomes true, it would be the second-highest fiscal deficit ever recorded, only behind the deficit of $232.5 billion in 2020-21. This would also mean that the Government's fiscal reserves might fall to just around $800 billion. The deficit would be more severe if the issuance of Green Bonds this year, amounting to $35 billion, has not been taken into account.

Since the beginning of this year, while the epidemic hit the economy, substantial tightening of monetary policies by central banks around the world has also seriously weakened the external economic momentum and impacted on the local economic situation. In light of weaker economic performance, we revised our forecast for Hong Kong's economic growth downward twice this year. With poorer performance in exports, private consumption and fixed investments, the business environment would be challenging, and revenues from profits tax and salaries tax in this financial year would likely be lower than the estimation earlier this year.

For stamp duties, the average daily turnover of the Hong Kong stock market between April and August this year was $117 billion, representing a year-on-year drop of 26%. Residential property transactions for the first four months of this year fell by 37%. Given the slackening stock and property markets, revenue from stamp duties might be one-third less than originally estimated.

Amid a sluggish property market, revenue from land premium for the first five months of this financial year amounts to $17.2 billion, which is far below the annual estimated revenue of $120 billion. Judging from past experience, land premium would be prone to larger adjustments as property prices went down. In April, tendering was unsuccessful for a residential site. In a slackening economy, the market demand for commercial sites would also weaken, and developers would be less interested in initiating land premium negotiations. All these have affected our land revenue.

At the same time when government revenue is falling, expenditure is increasing significantly. Faced with the epidemic and the downward pressure on the economy, we have been implementing various counter-cyclical measures to cope with economic contraction and uphold market confidence. Taking into account the counter-cyclical measures totaling more than $170 billion in the Budget at the onset of the year alone, it was estimated that a deficit of over $56 billion would be recorded for this financial year. Nevertheless, the figure has yet reflected the “Employment Support Scheme 2022” which was subsequently rolled out, costing $43 billion, and measures under the sixth round of the Anti-epidemic Fund.

In short, with falling revenue and rising expenditure; a complex and volatile external political and economic environment; and a bumpy road to global economic recovery, the economic prospect of Hong Kong is filled with challenges. Making good use of public monies to support the grassroots and people's livelihood, and to maintain the stability of the society, is a priority for us in the short to medium term. In capitalist markets, it is not easy to strike a proper balance between maintaining competition and letting the market exert its force on the one hand, while on the other helping businesses to survive. In introducing support measures, we must also take into account fiscal robustness and appropriate use of public monies. As financial resources are scarce, while reserving sufficient resources for what needs to be done, we must maintain fiscal robustness and sustainability to ensure economic security and financial stability.

The outlook for our economy in the next few quarters remains highly challenging. The second round of consumption vouchers to be disbursed on 1 October will inject more than $15 billion of purchasing power into the market, stimulating the economy with a multiplier effect. However, the key to improving our economy is better control of the epidemic, and convenient cross-boundary travel is at the heart of reigniting the economic momentum. The Government has continued to call on everyone to get vaccinated so that we can build a solid barrier against the epidemic together. This is the most effective way to protect ourselves and the health of our relatives and friends. It will help us strive for the resumption of normal economic activities and external connections, which is essential to securing our livelihoods and promoting strong economic growth in Hong Kong.

September 18, 2022