Blog

Financial security amid violent acts and the pandemic

It was my first time to give a comprehensive overview of our work on ensuring Hong Kong’s financial security at the National Security Education Day forum last year. I revisited this topic at the same occasion this year, as many raised concerns over the issue in view of the social incidents in the past months and the recent COVID-19 pandemic, both of which have caused a severe blow to the economy and the financial market. These incidents have provided a stress-testing scenario for our regulatory and responding mechanism for ensuring financial security. In short, the market remains its orderly operation despite market turbulence, which proves the effectiveness of our coordinated mechanism for safeguarding financial security across markets which operates around-the-clock.

In summary, the work on ensuring Hong Kong’s financial and economic security over the past year focused on three major aspects, including (1) to prevent speculative activities which might affect the stability of the Hong Kong dollar exchange rate; (2) to ensure adequate liquidity in banks and relieve the cash flow pressure of enterprises for protecting our economy and banking system from capital chain rupture; and (3) to monitor the changes in the asset market and related activities for ensuring the orderly operation of the financial and asset markets.

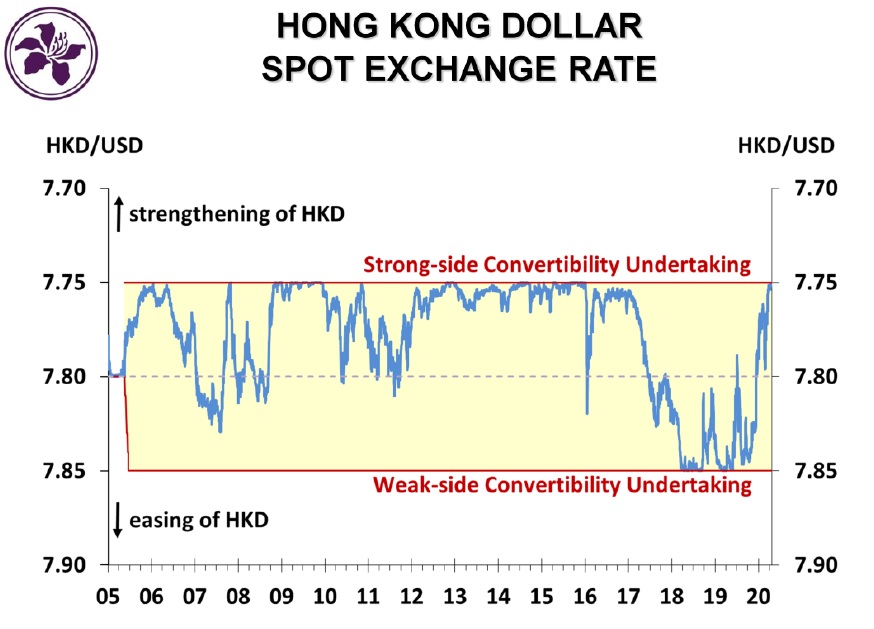

Although the market confidence was once damaged by the social incidents and violent acts since last June, this did not lead to large-scale capital outflow. Such outflow was not seen during the recent COVID-19 pandemic despite the pressure faced by the stock market along with the external environment. On the contrary, the Hong Kong dollar exchange rate has continued to be strong recently, staying close to the strong-side Convertibility Undertaking (CU) of HK$7.75 against the US dollar under the Linked Exchange Rate System (LERS). In fact, the strong-side CU has been triggered several times, reflecting a net capital inflow into Hong Kong. As of last Thursday (April 23), the Hong Kong Monetary Authority (HKMA) had undertaken US dollar selling from the market four times and had released a total of HK$7.71 billion of funds, further increasing the aggregate balance of Hong Kong’s banking system to HK$66.8 billion. This is part of the normal and automatic operation of the LERS, ensuring the hovering of Hong Kong dollar exchange rate within the target range of 7.75 to 7.85.

The LERS plays a role in maintaining the stability of the Hong Kong dollar exchange rate under either scenarios of capital inflow or outflow, forming a solid basis for market confidence towards the LERS. Moreover, our abundant foreign exchange reserves could readily meet the exchange needs in case of capital outflow. Confidence is the basis of the whole mechanism while our reserves back up the confidence. These effectively prevent over-speculation on Hong Kong dollar and consolidate the stability of the Hong Kong dollar exchange rate.

Despite the recent continuous capital inflow into Hong Kong, there have been no large-scale speculation or market-manipulating transactions so far. Since the global financial crisis in 2008, there has been a capital inflow of HK$1,000 billion into Hong Kong, most of which has remained here with only less than HK$140 billion flowed out of Hong Kong so far. As such, interest rates in Hong Kong have also been hovering at low levels. In fact, the Hong Kong dollar is freely convertible, and there is free flow of capital with no foreign exchange control in Hong Kong. Nevertheless, the Hong Kong dollar exchange rate has remained stable under the effective operation of the LERS, and the Hong Kong dollar market has always been operating smoothly and orderly. In other words, even if there is a net capital outflow in the foreseeable future, and if the exchange rate of the Hong Kong dollar weakens or even touches the weak-side CU of HK$7.85 against the US dollar, our long-standing LERS will continue its effective operation in sustaining the stability of the Hong Kong dollar exchange rate. In fact, the weak-side CU was triggered multiple times between April and August 2018. While there were some worries, the operation of the LERS was proven to be effective, and the Hong Kong dollar exchange rate was maintained within the designated range. This effective mechanism maintains the market confidence on the LERS, which is of utmost importance to the stability of Hong Kong’s economy and people’s livelihood.

|

In fact, the scale and flow of Hong Kong dollar capital in the market not only associate with the fluctuation of the Hong Kong dollar exchange rate, but also affect banks’ liquidity and readiness to offer loans. This could put pressure on the cash flow of enterprises, which relates to the second major aspect of our work on financial security as mentioned above. The recent pandemic has caused a sudden freeze in economic activities and capital chain rupture in some enterprises. In the event of enterprises winding off and laying off staffs, people’s livelihood and the banking system could be affected.

To ensure the liquidity of banks and space for offering loans, my colleagues at the HKMA and I have been putting forward various measures to ensure the availability of Hong Kong dollar, US dollar and internal resources of banks, with a view to facilitate banks in actively offering loans to enterprises to ride over the current challenges. This topic has been covered in my earlier blog entry. As for the concessionary low-interest loan with 100 per cent government-guarantee commitment announced in the Budget for easing the capital flow challenge of enterprises, 180 applications were approved in the first four days upon the launch of the scheme, involving over HK$400 million.

With regard to the financial and asset markets, I have been leading the Council of Financial Regulators in the “cross-market, coordinated, and around-the-clock” monitoring of the market. The financial regulators have been working closely together to monitor the fluctuations in currencies, stocks, futures and derivatives markets, and analyse the nature of such activities, including short-selling, speculation, and cases of concerted actions. To ensure normal operation of the market, we have, over the past year, increased the deposit requirement for the stock market, reduced the leverage risk of the spot market, conducted multiple rounds of stress tests, and enhanced on-site inspections of market players. As for the real estate market, rounds of prudent macro-demand management measures have been in place, while there is still an overall shortage in housing supply. Although the property prices are currently at a hardly affordable level, the risk of a dramatic fall in the residential property market is limited.

To sum up, although the COVID-19 pandemic has posed pressure on the global and local economy and the financial market, the financial risks in Hong Kong are still manageable. The HKSAR Government will continue to strive to safeguard Hong Kong’s financial security, which is part of the important gatekeeping work for ensuring national security.

April 26, 2020