Blog

iBond 2020

While time may feel like passing slowly in 2020 to some people, it actually flies. The COVID-19 and the anti-epidemic measures have brought great difficulties and challenges to citizens and enterprises, as well as the society and the economy. In the blink of an eye, we are entering the last quarter of 2020. Looking back at the past nine months, there were "grey rhino" and "black swan" that sent shock waves to the financial markets. Yet amid the volatile global situation, Hong Kong's financial system has continued to operate in a stable and orderly manner.

|

The stability of the financial system is of utmost importance to the economy and people's livelihoods. The financial services sector is one of our pillar industries which contributes to about 20% of our GDP. It serves the real economy by facilitating the development of different sectors and addressing the operation and financing needs of enterprises. While the development of the financial market could help drive up the economy, it would be even better if citizens could take part in the process and benefit from it. With this consideration, I announced the relaunch of the inflation-linked retail bond (iBond) in the Budget earlier this year. The preparatory works are all ready and we are going to announce the issuance details very soon.

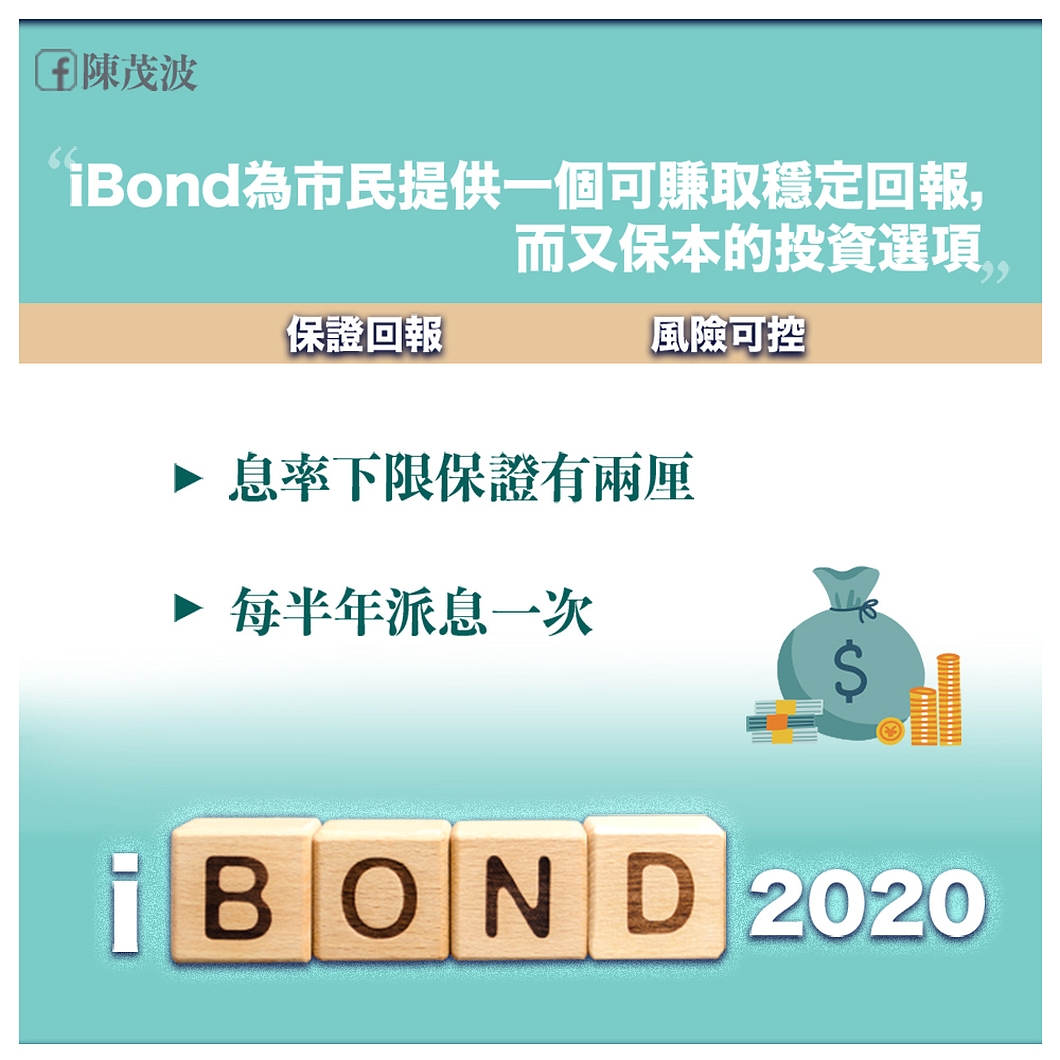

So why is the issuance of the iBond could allow the general public to have a greater involvement in the development of the financial market? The first batch of iBond launched in 2011 has attracted over 150 000 applications, which rose to over 500 000 by 2016. The total issue size during the 6-year period amounted to $60 billion. Compared with other retail bonds also issued by the Government before the iBond, only around 35 000 applications were received with an issue size of $7.5 billion in total. This shows the popularity of the iBond among citizens. The issuance of the iBond indeed does not only facilitate the development of the retail bond market, but also offer a capital protected investment option with stable return to the general public.

Given the current low inflation rate and even the possible risk of deflation in Hong Kong, some may question the attractiveness of the relaunch of the iBond. In fact, the global low interest rate environment will very likely persist for a period of time, and we should not overlook the risk of inflation in the medium-to-long term due to the easing of monetary policies in major overseas markets. Against this backdrop, the design of the iBond could take care of both scenarios. If the Composite Consumer Price Index (CPI) turns out to be negative, the guaranteed minimum interest rate of the iBond could ensure that the return would not become zero even under deflation. Taking into account the current situation, we have enhanced some of the conditions of this batch of iBond, including the minimum interest rate, which will be set at 2%, higher than that of the previous batches. This rate is quite attractive under the current low interest rate environment. If inflation occurs, the interest of the iBond will be linked to the Composite CPI, ensuring a return which could catch up with the inflation.

In fact, the structure of the iBond is easy to understand, such as the semi-annual interest payments with an interest rate linked to the average annual inflation rate based on the Composite CPI. Principal will be repaid in full at maturity. This product has opened up a channel for small investors to invest in bonds. After the issuance of this batch of iBond, we are going to launch the Silver Bond which targets at people aged 65 or above. The total issue size of the two types of bonds would be up to $13 billion. If the bonds are well received, we could consider issuing more.

The issue of different types of bonds in Hong Kong, including iBond, Silver Bond, or other retail bonds by the Ministry of Finance of the Central Government or other enterprises, can facilitate the effective allocation of capitals, provide people with more investment options after taking into account their own risk appetite, and promote the further development of the bond market in Hong Kong.

October 4, 2020