Blog

Milestones of Mutual Market Access

Since the beginning of the reform and opening up of our country, Hong Kong’s capital markets have seen extensive and profound developments. Through continuously developing and enhancing our financial infrastructure, building an international capital and talent pool, and upholding an innovative spirit, we have served the needs of our country in different development stages with our efficient and flexible market as well as innovative and diversified financial services and products. In the process, Hong Kong has also developed as our country’s international financial centre and sustained the development of our economy.

Looking back at the development process, it essentially comes down a few points: finding the right direction, firmly pressing ahead, steadily moving forward and continuously deepening development. Taking mutual access between Hong Kong’s and Mainland’s capital markets as an example, banks in Hong Kong commenced personal Renminbi (RMB) business in 2004, which has since then been constantly developed and expanded to cater the needs for exchange and cross-boundary trade settlement by enterprises. In 2014, the Shanghai-Hong Kong Stock Connect was launched, which offered for the first time a channel for investors and enterprises to directly participate in the stock markets of the two places. Subsequently, mutual access has continued to deepen gradually – from Shanghai-Hong Kong Stock Connect to Shenzhen-Hong Kong Stock Connect, from stocks to bonds, from spot market to derivatives market – providing international and Mainland investors with more diversified investment choices and risk management tools. Following the successful implementation of various mutual access schemes between the markets of both places, an onshore trading model under prudent risk management has been created, beneficial to both onshore and offshore investors. It has also generated unprecedented cross-boundary market liquidity and vibrancy while supporting the opening up of our country’s financial markets in an orderly manner. Such development will be accelerated by further expansion of mutual market access arrangements, announced last Friday by the China Securities Regulatory Commission (CSRC) – certainly a piece of good news in respect of deepening the development of Hong Kong’s capital markets. For this, the HKSAR Government is truly grateful.

|

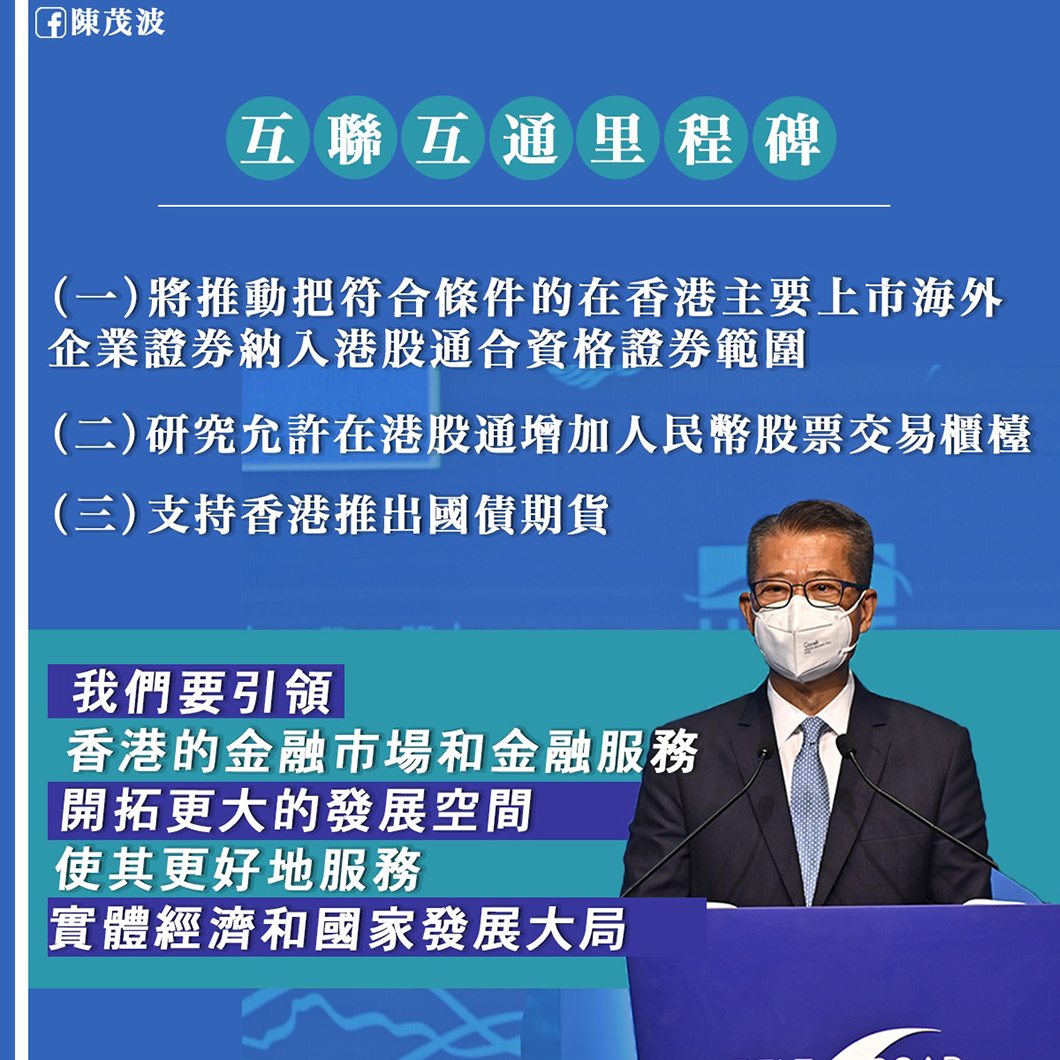

Vice Chairman of CSRC, Dr Fang Xinghai, said last week that CSRC would (a) move forward to include securities of overseas enterprises that have primary listing in Hong Kong and fulfil certain conditions in the eligible scope of Southbound Trading of Stock Connect; (b) study the setting up of an RMB securities trading counter under Southbound Trading of Stock Connect; and (c) support the issuance of Mainland government bond futures in Hong Kong.

So how significant are these three measures to the development of Hong Kong’s capital markets?

First, moving forward to include securities of overseas enterprises that are primary listed in Hong Kong and fulfil certain conditions in the eligible scope of Southbound Trading of Stock Connect. This measure would allow Mainland investors to invest in the stocks of relevant overseas companies through Southbound Trading of Stock Connect while ensuring proper risk management. It would improve the liquidity and valuation of relevant securities, and is thus conducive to attracting more quality and high-profile overseas enterprises with close business connections with the Mainland to list in Hong Kong. It would also enhance Hong Kong’s competitiveness and distinctiveness as our country’s international financial centre, while facilitating further high-quality opening up of the Mainland’s financial markets.

Second, setting up an RMB securities trading counter under Southbound Trading of Stock Connect. The measure would “kill two birds with one stone” – lowering the exchange rate risk and cost of Mainland investors on the one hand, while on the other enriching RMB investment choices in Hong Kong. It would help increase the liquidity and depth of the offshore RMB market. The two-currency option for buying shares would also provide investors with greater trading flexibility and incentives. The working group set up to this end – announced in the Budget earlier this year – has already been making preparations to overcome possible technical challenges, including setting up a “dual-counter market maker” regime as well as waiving the stamp duty on stock transfers by market makers in their transactions, so as to increase the liquidity of RMB-denominated stocks. It is our plan to introduce the relevant legislative amendments to the Legislative Council this year.

Third, supporting the issuance of Mainland government bond futures in Hong Kong. It offers another effective risk management tool for investing in Mainland government bonds through the Bond Connect and other channels. Together with mutual access arrangements for Swap Connect as promulgated earlier, overseas investors could hedge against changes in interest rates on RMB assets. By facilitating Hong Kong and overseas institutions to better manage relevant investment risks, the measure would improve the liquidity and reduce the bid-ask spreads in the Mainland government bond market, thereby further enhancing international participation in and acceptance of the market. It would also be beneficial to the internationalisation of RMB and help Hong Kong develop itself into a more comprehensive offshore RMB hub and risk management centre.

Mutual access between the financial markets of the Mainland and Hong Kong has been deepening and expanding, and the three measures have signified a new stage of development. The Mainland is pressing ahead with two-way opening up and high-quality development of its capital markets. As our country’s international financial centre, offshore market outside the Mainland, and only financial centre maintaining the common law system and fully connected to international markets, Hong Kong, and our capital markets, are at a new starting point. We need to be innovative and willing to embrace change, and to proactively align ourselves with the development strategy and needs of our country. We will also need to broaden the development of our financial markets and services so as to better serve the real economy and national development. We are all the more determined to make important and irreplaceable contributions to Hong Kong and our country.

September 4, 2022