Blog

Hong Kong Economy in 2021

As the leaves fall, we are already through most of the year 2021. Some described this year as a “Year of Recovery” for the economy, as most economic indicators have continued to improve so far this year. This uptrend has been powered by very strong exports of goods in the first half of the year, followed by renewed momentum in fixed investment and sustained improvement in private consumption expenditure.

Alongside the roll-out of mass vaccination programme around the world, the global anti-epidemic work has entered into a new phase. The successive reopening of some major economies together with the solid recovery of the Mainland economy have led to a sharp rebound in global demand. Against this backdrop, production and trading activities in Asia were robust. The value of Hong Kong’s total exports of goods surged by 30% in the first half of the year. While the growth momentum moderated afterwards, total exports of goods still posted a 22.7% increase in Q3.

|

The local epidemic was largely under control in recent months, and the public went out more to spend. The value of total retail sales in Hong Kong rose by 8.4% in the first half of the year, while total restaurant receipts also turned to a 0.5% increase. The disbursement of electronic consumption vouchers in the past few months further boosted sentiment in the retail and restaurant sectors. Retail sales rose by 11.9% in August, and the upcoming figures on retail sales and restaurant receipts should reflect the continued vibrant atmosphere in the market.

The economy grew notably by 7.8% year-on-year in the first half of the year, driven by strong export performance and the gradual revival of domestic demand. Advance estimates on GDP for Q3 will be released tomorrow (1 November). As the recovery of Hong Kong’s economy has become more entrenched in recent months as evidenced by trade and consumption-related indicators, I believe that the growth figure for Q3 would still be visible. However given the much stronger-than-expected rebound in the first half of the year and the higher base of comparison in the second half of last year, the year-on-year growth rate in Q3 should be lower than that in the first half.

The trend of sustained solid recovery in the economy is also witnessed in the latest labour market data. The seasonally adjusted unemployment rate declined sharply from a 17-year high of 7.2% at the beginning of this year to 5.5% in Q2, and further to 4.5% in Q3, which is the lowest level since Q1 of last year. Wage and payroll growth also accelerated slightly in Q2. Total employment in the retail, accommodation and food and beverage services sectors combined, which were hard hit by the epidemic, also bottomed out and rose by 3.5% year-on-year in Q3. In addition, business sentiment generally improved and augured well for the recovery of business investment activities.

Looking ahead to Q4 of this year, the growth rate of Hong Kong’s exports of goods will likely slow down as global economic growth has already shown signs of peaking out. Domestically, the performance of consumption-related sectors will continue to be supported by the improved employment and income conditions, as well as the effects of the Consumption Voucher Scheme. In mid-August, the Government projected the economic growth for 2021 as a whole to be 5.5% to 6.5%. Judging from the developments so far, I expect that the actual growth figure for the year as a whole should be close to the upper end of this forecast range.

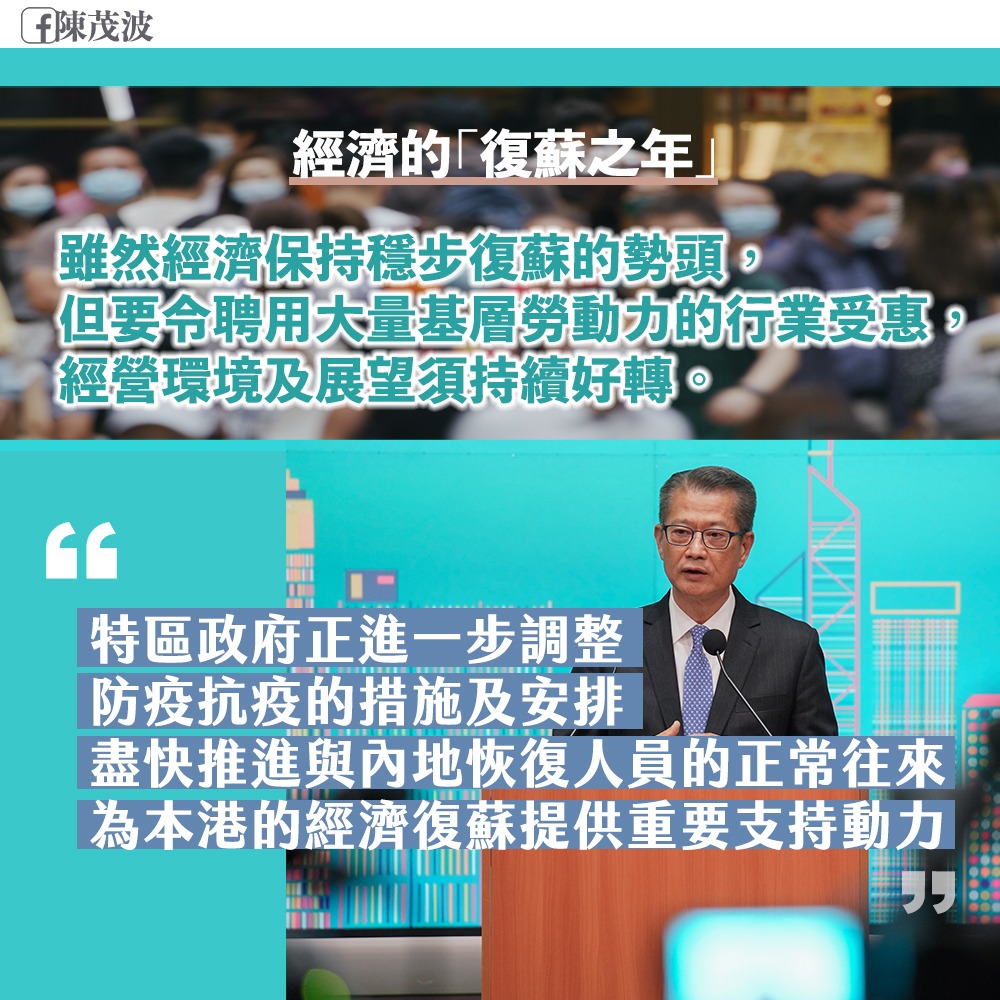

While the economy has stayed on a path of steady recovery, the business environment and outlook will need to improve continuously so as to benefit industries that employ a large number of grassroots workers. According to the Census and Statistics Department, the year-on-year increase in the average wage rate accelerated slightly to 1.1% in June this year. However, after discounting the changes in consumer prices as measured by the headline Consumer Price Index (A), the overall average wage rate still fell by 0.3% in real terms. To a certain extent, this figure reflected that even though the economy has continued to revive so far this year, the actual “sensory temperature” for the grassroots workers may still yet to warm up.

In addition, while the recovery trajectory of the Hong Kong economy has remained solid so far, we cannot overlook the risks lurking in the external environment. The more infectious Delta variant continues to plague many parts of the world. This, together with supply bottlenecks in many economies, have posed downside risks to the global economic outlook. Moreover, the elevated energy and commodity prices, rising shipping costs and heightened external inflationary pressures could also hinder global economic growth and also exert inflation pressures in Hong Kong. Changes in the monetary policies of central banks in the US and Europe, as well as China-US relations and geopolitical tensions also require attention.

Earlier, the International Monetary Fund (IMF) forecasted that global economic growth would decline from 5.9% this year to 4.9% next year. The IMF also pointed out that the momentum of the global economic recovery has weakened recently and the balance of risks is tilted to the downside. Therefore, we must stay alert. I will make a forecast for Hong Kong’s economic growth next year when I prepare the coming Budget.

Hong Kong’s socio-economic development has always been inseparable with our Country. Over the years, cross-boundary movement of people between the two places for business, trade, tourism, education or visiting relatives, has become an important part of our economic activities and daily lives. The HKSAR Government is further adjusting its anti-epidemic measures and arrangements with a view to resuming the normal flow of people with the Mainland as soon as possible, thereby providing a major impetus for our economic recovery. At the same time, Hong Kong is a business hub connecting the Mainland with the rest of the world. Many foreign companies in Hong Kong, including many foreign financial institutions, have operations in the Mainland. Resuming quarantine-free travel with the Mainland could facilitate their staff to visit and conduct business in the Mainland, which is very crucial for Hong Kong to uphold our hub status.

October 31, 2021