Blog

The Right Policy at the Right Time

The Hong Kong economy has been under pressure for the past one and a half years due to the social incidents and COVID-19 pandemic. Although the pace of contraction has moderated somewhat recently, the market are still cautious about the economic outlook, mainly due to the impacts of the unpredictable global and local epidemic situation on people’s livelihood and commercial activities. It is also worrying that the latest wave of the pandemic is spreading swiftly in the community.

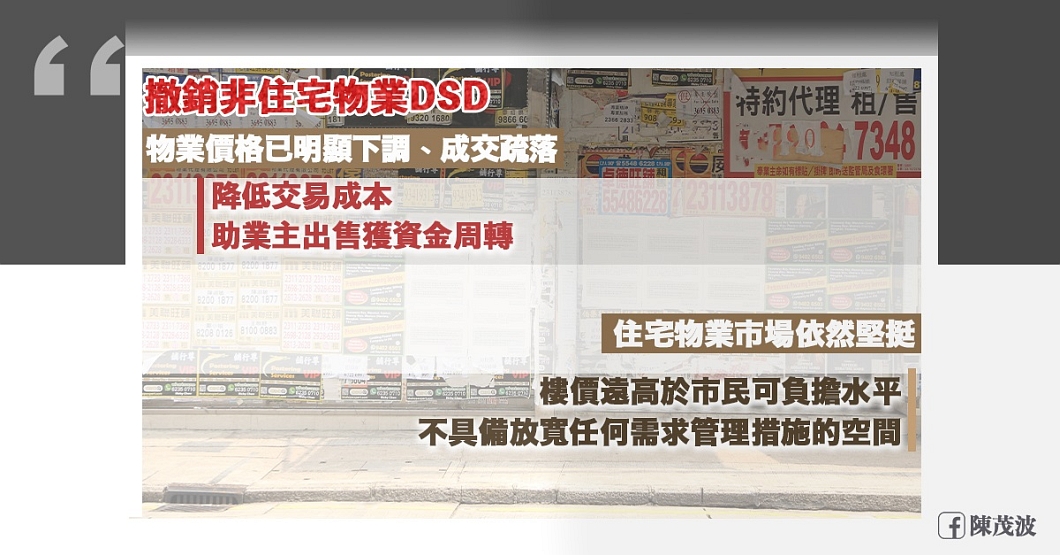

The shrinking economy and epidemic situation have made the operation of businesses very difficult. You may have noticed that more shops have become vacant in many areas while shopping recently, as has been the case for commercial buildings. According to data from the Rating and Valuation Department, prices of office space, retail shop space and flatted factory space have dropped by 19%, 17% and 13% respectively from their respective peaks in 2018 or 2019. Transactions of commercial property have been quiet over the same period. For instance, transactions of office space plunged from the high level of over 300 cases in the second quarter last year to the record low of 100 cases in the first quarter this year, while those of retail shop space also dropped from around 460 cases to less than 200 cases over the period. Many companies holding commercial properties may encounter difficulties if they wish to take out a mortgage loan or sell their property to meet urgent needs when facing operational or cash-flow pressures. As such, some have proposed to the Government the abolition of the Doubled Ad Valorem Stamp Duty (DSD) on non-residential property transactions, with a view to reducing transaction costs and facilitating property owners with financial difficulties to sell their property for liquidity.

|

In fact, the Government has rarely intervened in the non-residential property market in the past. Among the several rounds of demand-side management measures, only the DSD introduced in 2013 was applicable to non-residential properties. This is because for commercial properties, the Government respects the principles of free economy and is fully confident in the effectiveness of the market mechanism as the most efficient means to allocate resources in most situations. The Government will not intervene unless under exceptional circumstances, such as when there are excessive speculation activities in the market that could lead to potential risks in the macro-economy and the financial system. In 2012, when residential flat prices rose continually, prices of commercial properties also surged in parallel. The market showed clear signs of overheating, with prices of office space, retail shop space and flatted factory space risen by 25%, 41% and 46% respectively during the year. Therefore, when the DSD was introduced in 2013, the Government expanded its scope to include non-residential properties as well.

However, dented by the China-US trade tensions, the local social incidents and the COVID-19 pandemic over the past two years, the commercial property market has undergone a visible correction. The elevated prices and intense speculation activities at the time when the DSD was introduced are no longer evident. Taking the example of office space, prices have risen by a cumulative 21% since 2013 when the measure was introduced, similar to the rate of inflation over the same period, while prices of retail shop space have even declined by 1%. So far this year, transaction volume has dropped by around 80% to 90% from the level before the implementation of the DSD. Under the current economic environment, we believe the abolition of DSD for non-residential properties will unlikely lead to a revival of the intense speculation activities. This is the appropriate exit timing for the demand-side management measure. Abolishing the DSD would lower the relevant transaction costs and assist owners to sell their properties for meeting financial needs. Therefore, the Chief Executive announced this decision in the Policy Address delivered last week.

After the announcement of this decision, some commentators have mentioned whether there is also room for abolishing or relaxing the demand-side management measures for residential properties. While that is a natural question, we should first take a detailed look at the residential property market situation.

While the residential property market has undergone some consolidation recently due to the social incidents and epidemic, flat prices remain high given the firm end-user demand and the low interest rate environment. Flat prices have more than doubled that in 2010 before the demand-side management measures were introduced. Even when the Hong Kong economy registered negative growth for five consecutive quarters, flat prices only declined by less than 3% over the same period, reflecting the strength of the residential property market and that flat prices are still way over the affordability of the general public. These figures and trends all show that there is no room for relaxing the demand-side management measures for the residential property market at this stage.

As I have mentioned in my blog early last year, the Government shall exercise prudence when assessing whether the demand-side management measures on the private residential property market are still appropriate. The relevant framework and factors to be considered are still applicable now. The four factors include:

- The magnitude and pace of downward adjustment in property prices, including changes in the premium between primary property prices and secondary market property prices of the same district;

- Transaction volumes in both the primary and secondary markets;

- Future supply of residential properties, such as completion, number of units ready for sale and potential supply in the short to medium term;

- The overall economic situation and outlook, including local economic performance, employment situation, trend of interest rates and capital flow, as well as the external economic environment.

As always, we will continue to monitor the market situation closely and conduct dynamic assessments, but there is no need to designate hard indicators or timelines for the relaxation of the relevant measures.

November 29, 2020