Blog

Removing tax barriers to raise competitiveness

|

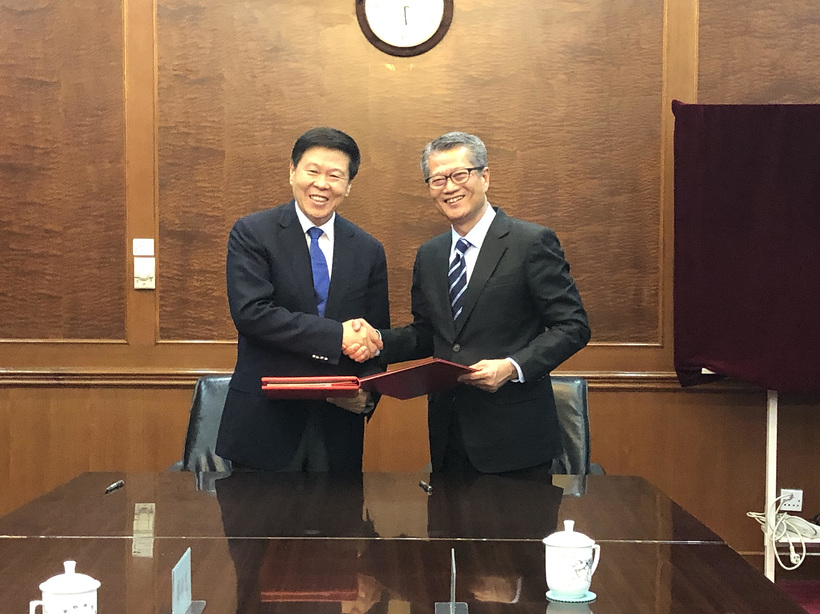

Two days ago, I went to Beijing to sign the “Fifth Protocol to the Arrangement between the Mainland of China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income” (“The Fifth Protocol”) with Mr Wang Jun, the Commissioner of the State Taxation Administration. One important measure covered by the Fifth Protocol is to provide tax exemption to qualified teachers and researchers, who is employed in Hong Kong or the Mainland and engages in teaching and research activities on the other side, for a period of three years, provided that the relevant income has been subject to tax on the side where the person concerned is employed. I believe this new measure will promote training, exchanges of talent and scientific research collaboration between the two places, and drive the development of the Guangdong-Hong Kong-Macau Greater Bay Area (GBA) to be an international innovation centre.

Collaboration in technology and scientific research between Hong Kong and the Mainland has been a dominant trend. Tertiary institutions in Hong Kong have already established twelve “industry, education and research bases” and graduate schools, as well as two campuses in the Mainland. With the Fifth Protocol coming into effect, teachers and researchers who have to travel across the border frequently would be benefitted.

With the implementation of the GBA development plan, economic cooperation between Hong Kong and other GBA cities will continue to be deepened, especially in the areas of scientific research and innovation and technology. Complementary development between cities and free flow of production factors facilitate the development of a vibrant ecosystem and a comprehensive industrial chain, leading to maximum synergy. Furthermore, human capital is the key to successful development. We must better collate the differences in tax systems within the area, so that talents could flow freely in the area without worries on tax matters, and that Hong Kong people can unleash their potential in a larger market.

At the same time, the GBA also provides tax concessions to high-end talents and talents in short supply. Last month, the Department of Finance of Guangdong Province and the Guangdong Provincial Tax Service under the State Taxation Administration made an announcement on tax concessions to high-end talents and talents in short supply working in the GBA. In short, for Hong Kong people working in the area, if their personal income tax payable exceeds 15% of their taxable income, the exceeded amount will be subsidised by the 9 municipal governments. The list and definition of high-end talents and talents in short supply are defined by individual municipal governments according to local needs, so as to ensure flexibility.

|

Besides, many Hong Kong people frequently travel to the Mainland for work over the years. Even though they are not residing in the Mainland, they make a long stay. Hong Kong people are therefore very concerned about their tax burden in the Mainland. In December last year, the State Taxation Administration announced the Regulations for the Implementation of the Individual Income Tax Law of the People's Republic of China, stipulating the taxation arrangement of individuals who have no domicile in the Mainland. In March this year, it was announced that any stay of fewer than 24 hours on a particular day of the Mainland will not be counted as “Day of Presence” in the Mainland while the definition of “Having Domicile” is further explained. In sum, it is a distinct tax concessionary measure for Hong Kong people to enjoy.

In general, according to the aforementioned regulations, if a Hong Kong person has no domicile in the Mainland, while his “Day of Presence” aggregated for 183 days or more in a year of assessment, if in each of the past six consecutive years, his “Day of Presence” does not exceed 183 days in the Mainland or there is single departure for more than 30 days, he is not required to pay individual income tax with respect to his/her income derived from sources outside the Mainland and paid by institutions or individuals outside the Mainland. Moreover, when there is a single departure for more than 30 days, his continuous years of residence in the Mainland would be recounted.

As for the calculation of “Day of Presence”, any stay of fewer than 24 hours on a particular day of the Mainland will not be counted. For example, if an individual arrives at the Mainland on Thursday and returns to Hong Kong on Saturday, his stay in the Mainland would be one day only (i.e. Friday) on taxation. This is an extremely attractive measure applicable to Hong Kong people working in the Mainland.

Apart from the Mainland, the HKSAR Government is committed to signing Comprehensive Double Taxation Agreements with more countries and regions in the world. These arrangements could reduce double taxation, facilitate the movement of goods, service trade and talents, attract investment, as well as encourage multinational and mainland enterprises to establish holding companies in Hong Kong when investing in other countries. Together with the current supporting measures, e.g. tax concessions for these enterprises’ corporate treasury centres in Hong Kong, we aim to develop Hong Kong as a hub for regional headquarters of enterprises outside Hong Kong.

Since its inauguration, the current-term Government has signed Comprehensive Double Taxation Agreements with India, Finland, Saudi Arabia and Cambodia. Hong Kong so far has signed 41 Agreements in total, in which 13 are signed with Hong Kong’s 20 largest trading partners. We will continue to expand this network proactively to develop Hong Kong as a more competitive springboard for overseas investment and the first-choice platform for regional headquarters.

July 21, 2019